WanStone Capital Flagship Investment Framework

Our flagship investment framework integrates a macroeconomic model with market risk regime measurements. This framework is represented visually by the Map.

At the core of our investment theory is the recognition that different asset classes offer varying risk-return profiles across distinct phases of the economic cycle and under different market risk regimes.

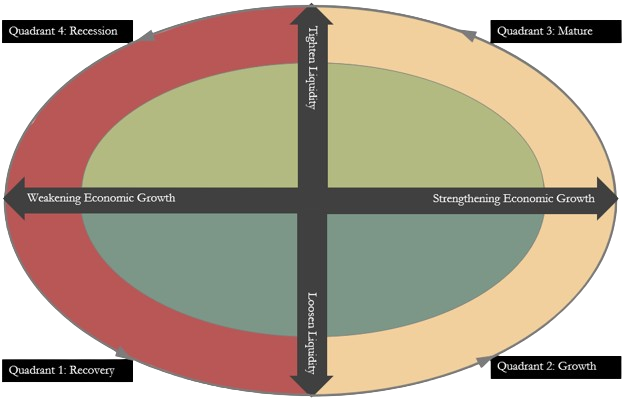

A typical economic cycle progresses through four phases: Recovery, Growth, Mature, and Recession, each corresponding to a quadrant on the Map. Our quantitative macroeconomic model dynamically identifies the current phase by algorithmically analysing a curated set of macroeconomic indicators. Our model precisely locates the market within one of the Map's four quadrants.

Simultaneously, our market risk measurement model systematically evaluates short-term market trading volatilities and long-term market fundamental risks to determine current market risk regime, which correspond to the color-coded zones on the Map (Green, Light Green, Yellow, and Red). The risk model determines which colour zone of the Map the market occupies.

By synthesizing signals from the macroeconomic model (quadrant positioning) and the risk model (colour coding), our investment framework accurately determines the market's position on the Map at any given time.

The positioning on the Map determines how much risk the portfolio should undertake and which risk premium factors the portfolio should exploit, and ultimately drives portfolio asset allocation and investment selection decisions.

The Map

The Edges of Our Investment Framework

What makes our investment framework standout?

Our investment framework is driven by time-tested economic theories based on macroeconomic data:

Being boxed within well-established economic theories reduces the risk of data mining;

Economic patterns are more stable and more likely to repeat themselves than are asset pricing patterns;

The strategy is easy to understand and get buy-in from investors.

The said economic theory is widely exploited by the market, how does our investment framework outperform others?

The well-studied economic theories can be looked at as a map. Some use the map and make judgments to determine where they are and which direction they should take.

In contrast, our investment framework can be looked at as the GPS signal, the blue dot on the map, that can objectively pinpoint where we are and which direction we should take.

Whilst some apply the economic theories discretionary when making investment decisions, our investment framework quantitatively analyses a wide range of dynamic economic data and linking it to the financial market to support structured and objective investment decision making.

Knowing the economic theories (having the map) is nothing special but being able to objectively apply the economic theories to turn data into actionable investment decisions (being able to repeatably generate accurate GPS signals on the map) is the edge.

And compared with other quantitative economic models, our investment framework has proven its accuracy via over a decade of live history covering multiple economic cycles.

Investment Theory: Different asset classes present different risk/return profiles when the market is in different phase of an economic cycle (different quadrants on the Map) and within different risk regimes (different colour zones on the Map).

The quantitative investment framework systematically and dynamically pinpoints where we are on the Map (quadrants and colour zones) based on on-going economic and market risk data.

The dynamic positioning on the Map determines the level of risk we target and the different risk factors we allocate to.

The level of risk can be managed by adjusting the high level asset allocation in the case of a long-only multi-asset strategy, or by managing the long-short ratio for an absolute return equity strategy.

Targeting different risk factors is through sub-level portfolio construction.